Rural Prosperity

Rising Rural Incomes and Upbeat Sentiments

प्रविष्टि तिथि:

31 JUL 2025 13:34 PM

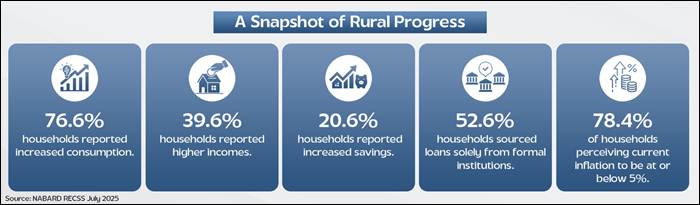

76.6% of rural households report increase in consumption in last one year

Key Takeaways

- Rural prosperity is rising, with 76.6% of households reporting increased consumption and 39.6% seeing higher incomes in last one year—both the highest across all survey rounds.

- Financial health is improving, with 20.6% of households reporting higher savings and 52.6% sourcing loans solely from formal institutions.

- Optimism is strong, with 74.7% expecting income growth over the next year and over 56.2% anticipating better job prospects in the short term.

- Government support and infrastructure upgrades—especially in roads, education, and water—continue to bolster rural resilience.

- Inflation concerns have eased, with over 78.4% of households perceiving current inflation to be at or below 5%, reflecting improved price stability.

Introduction

In a clear sign of rural economic momentum, the July 2025 round of the Rural Economic Conditions and Sentiments Survey (RECSS), released by NABARD recently, reveals that 76.6% of rural households reported an increase in consumption, marking a sustained trajectory of consumption-led growth. The RECSS serves as a vital tool to evaluate the real-world impact of various government schemes and rural development programmes. By capturing household-level data on income, consumption, credit, and sentiment, the survey offers valuable insights into how public welfare initiatives are translating into tangible economic outcomes on the ground. The findings paint an encouraging picture of rising incomes, expanding financial inclusion, and growing household optimism in rural India.

About NABARD

NABARD is India’s apex development bank, established in 1982 under an Act of Parliament to promote sustainable and equitable agriculture and rural development. This premier development financial institution has transformed lives in Indian villages through agri-finance, infrastructure development, banking technology, promotion of microfinance and rural entrepreneurship through Self Help Groups, Joint Liability Groups and more. It continues to aid in nation building through participative financial and non-financial interventions, innovations, technology and institutional development in rural areas.

Rising Incomes and Consumption-Led Growth

Income Growth

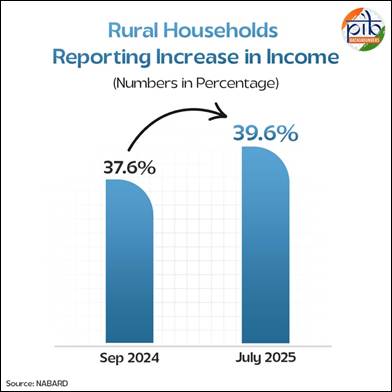

39.6% of surveyed households reported an increase in income during the past year—the highest share across all six rounds of the survey so far.

|

Income Increase Bracket (in %)

|

% of Households who reported Increase in Income

|

|

0–5%

|

24.7%

|

|

5–10%

|

42.5%

|

|

10–15%

|

14.9%

|

|

15–20%

|

8.9%

|

|

Above 20%

|

9.1%

|

Consumption Expenditure

- 76.6% of households reported a rise in consumption over the past year. Just 3.2% of households reported a decline in consumption, which is the lowest since this survey started.

- This growth is further reinforced by the highest recorded share of monthly income being spent on consumption at 65.57%, up from 60.87% in September 2024.

- This reflects enhanced purchasing power and stronger financial confidence of rural households.

Government Support Remains Crucial

Income and spending levels continue to be strongly supported by several fiscal transfer schemes, in both kind and cash, both from the Centre and states. These include subsidies on food, electricity, cooking gas, fertilizers, and support for school needs, transport, meals, pensions, and interest subsidies. On average, these transfers made up about 10% of a household’s monthly income. These interventions significantly enhance household resilience and reduce financial pressure, especially for vulnerable populations.

Strengthening Financial Health through Increased Savings

- 20.6% of households reported a rise in financial savings, showing a notable improvement in saving capacity alongside rising incomes.

- The reported share of income allocated to savings stood at 13.18%, while loan repayments accounted for 11.85% of household spending.

- Together, these numbers point toward a stronger culture of saving and debt management, alongside consumption growth.

Strong Sentiments on Income and Employment Outlook

Short-Term Sentiments (Next One Quarter)

- 56.4% of rural households expect income levels to improve in the next quarter, the highest across all rounds of the survey so far.

- 56.2% of rural households anticipate better employment opportunities in the next quarter, reflecting growing optimism across income-generating avenues.

- These values reflect a broad-based optimism about the near-term economic outlook in rural India.

Long-Term Sentiments (Next One Year)

- An all-time high 74.7% of rural households expect their income to increase over the next 12 months.

- This reflects a strong sense of confidence and forward-looking positivity, bolstered in part by a favorable monsoon and improving infrastructure.

The July survey also showed better perceptions of infrastructure, with only 2.6% of households reporting any decline reflecting growing satisfaction with basic services like roads, electricity, water, education, and healthcare.

Expanding Financial Inclusion and Formal Credit Usage

Shift to Formal Lending Channels

- Driven by continued policy efforts to promote financial inclusion, rural households increasingly rely on formal institutional sources for credit. A record 52.6% of households reported sourcing loans exclusively from formal financial institutions—banks, cooperatives, NBFCs, MFIs, etc.

- Another 26.9% borrowed from both formal and informal sources.

- This represents a strong shift away from unregulated lenders, ensuring better borrower protection and reduced cost of credit.

Decline in Informal Interest Burden

- The mean interest rate on informal loans declined to 17.53%, a 30-basis-point drop from the previous round.

- Despite being outside the formal system, 30% of rural households paid no interest on such loans—primarily due to borrowing from friends and relatives, indicating community-based financial support.

Rural Infrastructure Perceived to Be Improving

- 76.1% of households assessed that rural infrastructure improved over the past year.

- This reflects consistent progress in areas such as roads, electricity supply, drinking water, health services, and educational institutions.

Rural Development Priorities: Roads, Education, Water

Households were asked to rank areas where they noticed the most improvement in recent years. The top-ranked sectors were:

|

Rank

|

Area of Development

|

% of Households Ranking It 1st

|

|

1

|

Rural Roads

|

46.3%

|

|

2

|

Education Facilities

|

11.2%

|

|

3

|

Drinking Water Supply

|

10.0%

|

|

4

|

Electricity

|

8.6%

|

|

5

|

Health Infrastructure

|

7.5%

|

These rankings indicate that connectivity, education, and access to basic utilities remain at the forefront of rural development efforts and have seen visible progress.

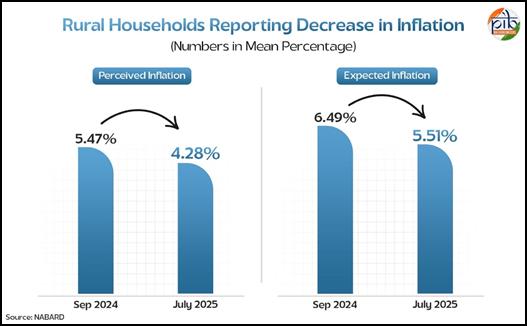

Declining Inflation Perceptions and Expectations

The CPI-rural inflation fell from 3.25% in March to 2.92% in April and further to 2.59% in May. Food inflation also dropped to 1.36% in May. In the July survey, rural households reported a lower inflation perception, averaging (mean value) 4.28%. A majority of households (78.4%) perceived inflation to be at or below 5%, while next-quarter expectations fell to a record low of mean 4.29%. One-year-ahead expectations remained stable at mean 5.51%.

Stable Food Expenditure Patterns

- The share of food in total monthly consumption expenditure remained stable at a median value of 50%, even with softening rural food inflation.

- This indicates that rising incomes are being used to diversify spending, without increasing pressure on food budgets.

Comparison of Key Parameters with Round 1 (September 2024)

|

Parameter

|

Sep-24

|

Jul-25

|

What This Means

|

|

Income increased (% of Households)

|

37.6

|

39.6

|

More families are earning better—income growth is picking up.

|

|

Consumption increased (% of Households)

|

80.1

|

76.6

|

A slight dip, but still high—people are spending more, which keeps the economy active.

|

|

Employment Outlook Next Quarter (% of Households reporting an increase)

|

52.6

|

56.2

|

Hope is growing—more households expect job opportunities to improve soon.

|

|

Income Outlook – 1 year (% of Households reporting an increase)

|

70.2

|

74.7

|

A big jump in confidence—people believe their incomes will rise over the next 12 months.

|

Conclusion

The July 2025 RECSS survey highlights strong growth and optimism in rural India. Incomes and consumption are rising, savings have improved, and more households are accessing formal credit. Sentiments about future income and employment are at their highest levels yet. Government support remains steady, infrastructure is improving, and inflation perceptions are at a record low. Overall, the rural economy is on a confident and upward path.

References

NABARD

RECSS July 2025:

https://www.nabard.org/auth/writereaddata/WhatsNew/1107255607RECSS%20Report%20of%206th%20Round%2009%20July%202025%20%20(1).pdf

RECSS September 2024: https://www.nabard.org/auth/writereaddata/tender/pub_0910240202031157.pdf

https://www.nabard.org/content.aspx?id=2

RT | SM

Difference between Mean Values and Net Values: -

Difference between Mean Values and Net Values

- Mean value: The average of all individual responses collected in the survey.

- Net value: The difference between the percentage of respondents reporting an increase and those reporting a decrease.

- Median value: The middle value in a sorted list of responses, where half the responses are above and half are below.

Rising Rural Incomes and Upbeat Sentiments

****

(तथ्य सामग्री आईडी: 149227)

आगंतुक पटल : 6073

Provide suggestions / comments

इस विश्लेषक को इन भाषाओं में पढ़ें :

हिन्दी