PIB Backgrounder

India’s Pension Landscape

Expanding Coverage, Ensuring Sustainability

Posted On:

07 MAY 2026 5:13PM by PIB Delhi

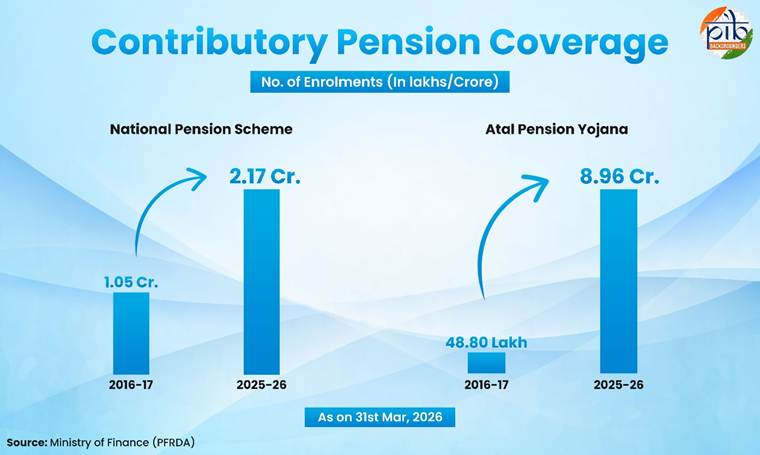

India transitioned from defined-benefit pension schemes to a diversified contributory framework. The shift promotes greater financial sustainability, shared responsibility and long-term retirement security. National Pension System (NPS) has over 2.17 crore subscribers, while Atal Pension Yojana (APY) reached 8.96 crore enrolments as on 31.3.2026. They are securing lives and supporting economic growth through large asset creation. The nation’s retirement system continues to expand with Assets Under Management reaching ₹15.95 lakh crore under NPS and APY assets at ₹51.4 thousand crore as on 31.3.2026. As India progresses, its pension system evolves through digital reforms and stronger governance.

|

Transforming Pension Systems for Inclusive Old-Age Security

With rising life expectancy and increasingly diverse employment patterns, strengthening retirement security has become an important public policy priority. In this context, India’s pension system has evolved significantly over time, shaped by successive policy decisions and institutional reforms. What was largely a defined-benefit arrangement for Government employees has expanded into a broader framework. It now includes contributory schemes and targeted social support for senior citizens. There is also more focus now on expanding social security coverage and improving service delivery through digital platforms. Administrative efficiency has also improved to support old-age income security.

What is Pension?

A Pension provides a steady monthly income to people during their unproductive years. Declining earnings, rise of nuclear families, migration of earning members, rising living costs and longer lifespans weaken financial security. Pensions ensure a dignified and independent life.

|

|

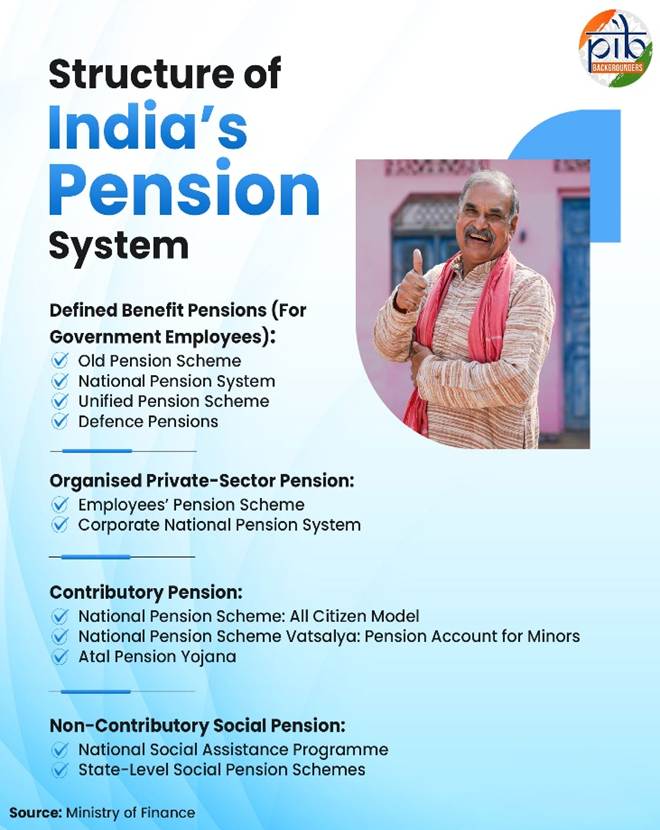

Pension Architecture in India

|

India’s pension architecture comprises a diverse set of schemes designed to provide income security to different segments of the population. It includes various components that operate under distinct funding mechanisms, eligibility criteria and benefit structures.

- Defined benefit pension systems for eligible Government employees, which guarantee a fixed post-retirement income.

- Contributory pension arrangements where individuals or/and employers contribute to retirement savings.

- Statutory payroll-linked schemes for organised private-sector workers that mandate employer and employee contributions.

- Tax-funded social assistance pensions, which support elderly, widowed and vulnerable individuals with limited or no formal income sources.

Defined Benefit Pensions for Eligible Government Employees

Government employee pensions have evolved from the budget-funded Old Pension Scheme (OPS) to contributory and revised arrangements.These include the National Pension System (NPS) and the recently introduced Unified Pension Scheme (UPS). However, Defence pensions, continue under separate provisions.

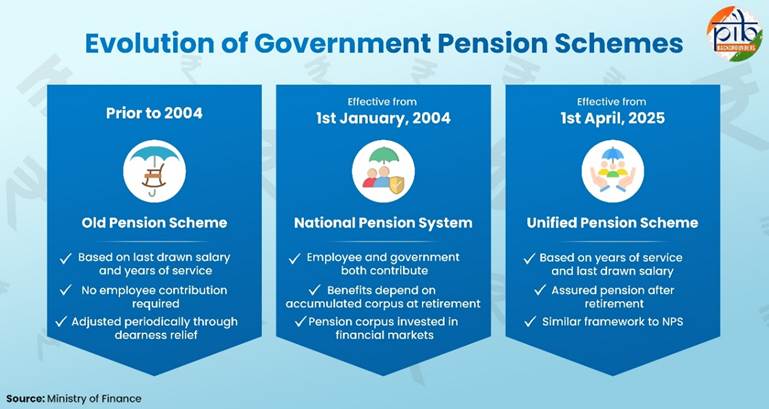

From CCS to UPS: Evolution of Government Pension Schemes

Prior to 1st January 2004, Central Government employees were covered under a defined-benefit, DA Indexed pension system. It was governed by the Central Civil Services (Pension) Rules, 1972, commonly known as the OPS. Under this system, government employees were entitled to a guaranteed pension funded by the government after retirement. The pension was determined on the basis of the employee’s last drawn salary and length of qualifying service. State Government employees were covered under their respective State Pension Rules, which were broadly modelled on these provisions.

From 1st January 2004, the Central Government discontinued OPS for new entrants and introduced the NPS. It is a defined-contribution framework in which both employees and the Government contribute. NPS is regulated and supervised by the Pension Fund Regulatory and Development Authority (PFRDA). The retirement benefits depend on the accumulated corpus and annuitisation rather than a guaranteed payout. The scheme encourages long-term retirement savings through a structured and portable pension system. It also supports fiscal sustainability by moving towards a contributory pension framework. Most State Governments subsequently adopted the NPS for new recruits, although a few continued with defined-benefit arrangements.

|

Did you Know?

Accumulated Pension Corpus refers to the monetary value of the pension investments. These are accumulated in the pension account of a subscriber under the NPS.

|

More recently, Unified Pension Scheme (UPS) came into effect from 1st April 2025. It is an option under the National Pension System (NPS) for eligible Central Government employees covered under NPS and choose this option under NPS. The scheme follows a contributory structure, with contributions from both employees and the Central Government. UPS aims to provide assured and inflation-linked retirement income. It also addresses concerns related to longevity and income predictability. It is regulated by the PFRDA and is applicable to both serving and retired employees subject to specific conditions. To be eligible for benefits under UPS, an employee must have completed at least 10 years of qualifying service. In case of death of the employee after retirement, the legally wedded spouse is eligible for family pension/payout under UPS.

While both NPS and UPS have the objective of providing payout/pension, they have structural differences. For instance, under UPS, the Government contributes 10% (of Basic Pay + Dearness Allowance) along with an additional 8.5% to a pool corpus. Whereas NPS provides a 14% direct government contribution in the individual NPS account. Additionally, UPS offers an assured payout/pension subject to conditions, while NPS does not guarantee any assured payouts and depends upon market returns.

UPS also ensures a minimum assured payout/pension of ₹10,000 per month for eligible employees with at least 10 years of service, which is not available under NPS. Dearness Relief is also provided in UPS but not in NPS. This is similar to Dearness Allowance (DA) given to serving employees. In case of death after retirement, the legally wedded spouse, at the time of retirement, is entitled to 60% of the payout/ pension as family payout/pension. Whereas NPS benefits depend on the market returns and annuity selected.

In addition, UPS provides a lump sum amount at the time of retirement, calculated as 10% of monthly emoluments (Basic Pay + DA) for every completed six months of qualifying service. This is paid in addition to the pension benefits.

Key features of the UPS include:

(a) Provision of a minimum assured payout/pension after retirement to employee & thereafter family payout/pension to legally wedded spouse; and

(b) Pension/payout amount that is linked to the employee’s years of service and last drawn salary.

These provisions aim to provide greater income certainty and stability after retirement.

Overall, the system reflects a gradual shift from OPS to NPS, with UPS functioning as an optional alternative within this framework.

Defence Pensions: Separate Defined-Benefit Structure

Administered separately by the Ministry of Defence, defence pensions are financed through budgetary allocations from the Government. Reflecting the distinct service conditions and career structure of armed forces personnel, it is non contributory in nature. It has unique features like One Rank One Pension (OROP) and Disability pension provisions. OROP (2015) ensures defence personnel retiring at the same rank and service length receive equal pension. This applies irrespective of their date of retirement.

Organised Private-Sector Pension Framework

Pension coverage for organised private-sector employees is built around statutory, payroll-linked arrangements rather than budget-funded entitlements. It operates primarily through two mechanisms namely the EPS and the corporate model of the NPS.

Employees’ Pension Scheme (EPS)

The EPS is administered by the Employees’ Provident Fund Organisation (EPFO) under the Employees' Provident Funds and Miscellaneous Provisions Act. It forms the statutory foundation of pension coverage for organised private-sector workers. Introduced in 1995, it applies to employees in establishments covered under the EPF law and is funded through contributions. A portion of the employer’s EPF contribution is allocated to EPS and pension benefits are calculated based on pensionable salary and years of service. Unlike market-linked systems, EPS operates through pooled contributions. It provides superannuation, disability and family pension benefits to eligible members.

Corporate National Pension System

In addition to EPS, private employers may offer the corporate model of the NPS. Under this both employer and employee contribute to individual pension accounts. This is regulated by the PFRDA.

Corporate NPS functions as a defined-contribution system, where retirement benefits depend on the accumulated corpus rather than a fixed formula. While EPS remains the statutory base for eligible establishments, corporate NPS serves as a supplementary or alternative retirement savings option. It offers greater portability and investment choices.

All-Citizen Contributory Pension Mechanisms

To extend retirement savings beyond formal employment, voluntary contributory options are available. These include the NPS and the APY (Atal Pension Yojana) for individuals outside statutory payroll coverage.

The NPS all-citizen model extends pension access beyond formal employment. It allows voluntary enrolment within prescribed age limits, flexible contributions and choice of investment options. It operates through a two-tier account structure:

- Tier I, which is the primary retirement account with certain withdrawal restrictions and;

- Tier II, a voluntary savings account offering greater liquidity.

Subscribers can make flexible contributions subject to prescribed minimums. They can also choose investment options across asset classes, including government securities, corporate bonds and equities. It can be subscribed by any Indian Citizen (resident/non-resident/overseas citizen). NPS is an Individual Pension Account and cannot be opened on behalf of a third person. The applicant should be legally competent to execute a contract as per the Indian Contract Act.

NPS Vatsalya: Pension Account for Minors

NPS Vatsalya (2024) is a contributory pension scheme, designed specifically for minors. Under this scheme, parents or legal guardians can open and operate a pension account for a minor. The minor remains the sole beneficiary and the subscriber of the account. Contributions are made until the minor attains the age of majority. Thereafter, the account is seamlessly converted into a regular NPS account and operated by the subscriber.

The scheme promotes early retirement savings and long-term financial planning by enabling investments to accumulate over an extended time horizon.

Atal Pension Yojana (APY)

APY (2015) aims to expand pension coverage among workers in the unorganised sector.It covers workers not included under statutory social security schemes. It is a contributory scheme for low-income subscribers, with enrolment facilitated through banks and post offices.

Subscribers can choose a fixed monthly pension ranging from ₹1,000 to ₹5,000. The pension is payable from the age of 60 years. The required contribution is predetermined based on the selected pension level and the subscriber’s age at entry.

Non-Contributory Social Pension Framework

Non-contributory social pensions provide basic income support through tax-funded transfers to elderly individuals in informal employment who lack retirement savings. Unlike employment-linked pensions, they focus on preventing destitution, forming a vital social assistance layer within the pension system.

National Social Assistance Programme (NSAP)

At the Union level, NSAP is implemented across rural and urban areas to provide social assistance to eligible beneficiaries. NSAP provides financial assistance to the economically vulnerable individuals. States/UTs are encouraged to provide top-up of at least an equivalent amount to the assistance provided by the Central Government. This ensures that the beneficiaries avail decent level of assistance.

Did You Know?

As of August 2025, States/UTs have added top-up amount ranging from ₹ 50 to ₹ 3800/month per beneficiary under NSAP. This results in an average monthly pension of around ₹1,000 in most of the States/UTs.

|

State-Level Social Pension Schemes

Alongside central assistance under NSAP, the State Governments also implement independent or supplementary social pension schemes. These schemes allow states to enhance pension benefits in line with their fiscal capacity and policy priorities. They also enable states to expand social pension coverage to a wider group of vulnerable beneficiaries. It includes the elderly, widows and persons with disabilities.

Certain examples of state-funded pensions:

- Madhu Babu Pension Yojana in Odisha,

- Aasara Pension Scheme in Telangana, and the

- Mukhyamantri Vridhjan Pension Yojana in Bihar

|

Wide Pension Coverage in India

|

Pension coverage in India has expanded over the past decade, with rising enrolment across major Government-backed schemes. Regulatory improvements and the strengthening of digital systems have supported this growth. As the workforce continues to grow and diversify, expanding formal pension participation remains important. It is a key pathway to further strengthening the pension system.

- The NPS and APY together reflect strong and sustained growth in India's pension landscape. NPS enrolments exceeded to 2.17 crore subscribers as on 31.3.2026. The APY also expanded significantly. It reached 8.96 crore enrolments in the same period.

- The EPS has also demonstrated robust growth, with contributory membership expanding to 7.98 crore members as of April 2026. It reflects continued expansion in formal sector employment and compliance.

- The non-contributory social pensions form a significant layer of income support alongside contributory pension systems. As of April 2026, the central social pension component covers more than 2.92 crore beneficiaries. During the same period, State Governments covered over 1.41 crore beneficiaries.

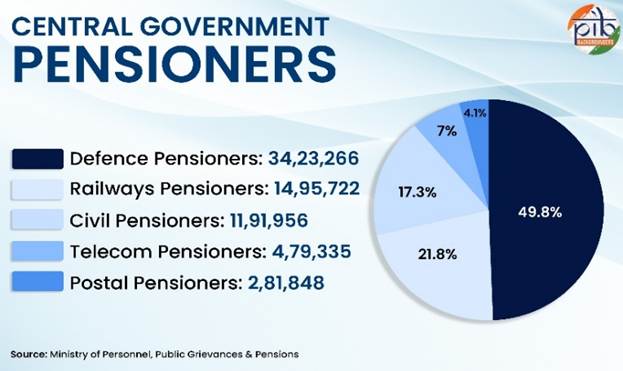

- A substantial segment of India’s pension landscape continues to be shaped by defined-benefit pension arrangements, paid to Central Government employees. It includes more than 34 Lakhs Defence and 14 Lakhs Railways pensioners.

|

Performance and Policy Reforms of the Pension Sector

|

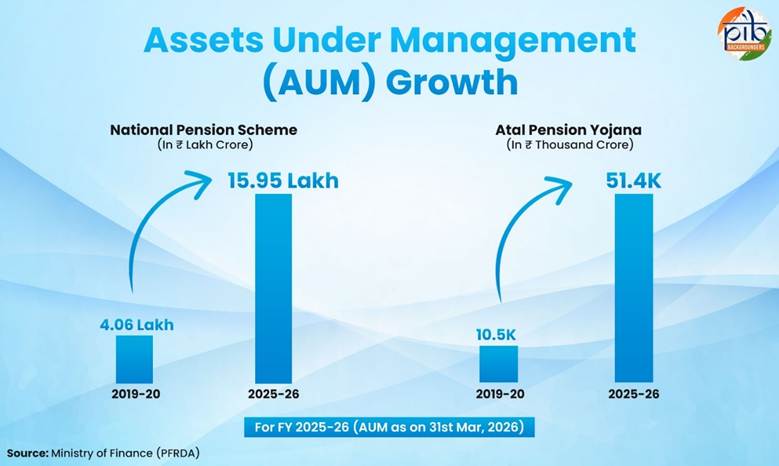

India’s pension system has also witnessed sustained asset growth, stable investment outcomes and strengthening institutional capacity.

As on 31.3.2026 Assets Under Management (AUM) under the NPS have expanded to approximately ₹15.95 lakh crore. The assets under the APY stand at around ₹51.4 thousand crore, reflecting steady corpus accumulation.

What is AUM?

AUM is a measure of the total market value of assets managed by a financial institution on behalf of its clients at any given point in time. These assets comprise equities, fixed income securities, cash and cash equivalents, mutual funds, real estate and alternative investments.

|

Alongside improvements in performance and asset growth, India’s pension system has also undergone sustained policy reforms. It aims at strengthening regulatory oversight, expanding coverage and improving institutional efficiency.

- Under the PFRDA, several regulatory initiatives have been undertaken to strengthen the pension ecosystem and enhance its efficiency and transparency. These measures include:

- Refinement of investment and compliance guidelines,

- Strengthening of supervisory and monitoring mechanisms and;

- Operationalisation of new pension frameworks such as the UPS.

- Balanced Life Cycle Fund (2024), is under the Auto Choice option of NPS. Itallows subscribers to maintain 50% equity exposure until age 45, as compared to 35 years age previously. It supports long-term growth during early working years while ensuring a gradual risk reduction thereafter.

- To expand pension participation beyond organised employment, several measures have been undertaken to improve access and enrolment among informal-sector workers. These include:

- Strengthening outreach and enrolment under the APY,

- Simplifying account opening through banking and post office networks and;

- Leveraging digital infrastructure to widen access to voluntary pension accounts under the NPS.

- Pension related provisions are covered in one of the new Labour Codes (2025). The Code on Social Security, 2020 provides enabling provisions to extend social security coverage. It includes pension-linked benefits to gig and platform workers, creating scope for future operational expansion.

|

Towards an Inclusive and Sustainable Pension System

|

India’s pension system has evolved into a multi-pillar framework. It includes contributory Government and private-sector schemes, voluntary citizen participation and non-contributory social pensions.

As demographic transition accelerates, retirement income security becomes vital for long-term stability. Wider coverage, prudent asset management and efficient service delivery are also essential. Ongoing policy and institutional evolution strengthen the pension system. It supports inclusive and sustainable old-age income security in the years ahead.

References

MINISTRY OF FINANCE

https://www.indiabudget.gov.in/economicsurvey/

https://npstrust.org.in/weekly-snapshot-nps-schemes

https://npstrust.org.in/apy-aum-and-subscriber

https://npstrust.org.in/aum-and-subcriber-base

https://npstrust.org.in/apy-aum-and-subscriber

https://npstrust.org.in/features-ups

https://npstrust.org.in/nps-state-governments

https://www.pib.gov.in/PressReleseDetailm.aspx?PRID=2174235®=3&lang=2

PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY (PFRDA)

https://pfrda.org.in/en/web/pfrda/

https://www.pfrda.org.in/web/pfrda/about-us/history

https://pfrda.org.in/documents/33652/146225/Annual%2BReport%2B2024-25%2BEnglish.pdf

https://www.pfrda.org.in/web/pfrda/intermediaries/registered-intermediaries/central-record-keeping-agency

https://www.pfrda.org.in/documents/33652/145901/Pension%2BBulletin%2BJuly%2B2025.pdf

https://www.pfrda.org.in/web/pfrda/w/regulatory-framework/circulars/active-circulars/introduction-of-balanced-life-cycle-fund-under-nps

https://www.pfrda.org.in/web/pfrda/schemes/national-pension-system/nps-for-all-citizen-models

https://www.pfrda.org.in/web/pfrda/schemes/atal-pension-yojana-apy

https://www.pfrda.org.in/web/pfrda/schemes/national-pension-system/nps-vatsalya

https://www.pfrda.org.in/web/pfrda/schemes/national-pension-system/nps-for-corporates

https://www.pfrda.org.in/en/web/pfrda/schemes/national-pension-system/about-nps

https://www.pfrda.org.in/web/pfrda/schemes/national-pension-system/nps-for-central-government

MINISTRY OF STATISTICS AND PROGRAMME IMPLEMENTATION

https://www.mospi.gov.in/uploads/publications_reports/publications_reports1770719506668_061eb34b-ec61-4890-9e61-73cc717b4d0b_Quarterly_Bulletin_PLFS_OCT-DEC_2025.pdf

MINISTRY OF DEFENCE

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2204165®=3&lang=2

https://desw.gov.in/en/pensions

https://www.pib.gov.in/PressReleaseIframePage.aspx?PRID=2071572®=3&lang=2

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2221612®=3&lang=2

https://desw.gov.in/en/pension-regulations

MINISTRY OF LABOUR & EMPLOYMENT

https://www.epfindia.gov.in/site_docs/Annual_Report/Annual_Report_2023-24.pdf

https://mis.epfindia.gov.in/ChartDashboard/

https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/EPS95.pdf

MINISTRY OF SOCIAL JUSTICE& EMPOWERMENT

https://india.unfpa.org/sites/default/files/pub-pdf/20230926_india_ageing_report_2023_web_version_.pdf

MINISTRY OF CHEMICALS & FERTILIZERS

https://jeevanpramaan.gov.in/v1.0/

MINISTRY OF RURAL DEVELOPMENT

https://nsap.dord.gov.in/nationalleveldashboardNew.do?methodName=nationalLevelInitial&val=temp&schemeCategory=ALL

https://nsap.dord.gov.in/nationalleveldashboardNew.do?methodName=getStateData&schemeCategory=S&main=notmain

https://nsap.dord.gov.in/circular.do?method=aboutus

MINISTRY OF PERSONNEL, PUBLIC GRIEVANCES AND PENSIONS

https://doppw.gov.in/en

https://pensionersportal.gov.in/FAQ-pension.aspx

https://cag.gov.in/uploads/media/CCS-Pension-Rules-1972-as-from-DoPT-website-20200717165308.pdf

https://pensionersportal.gov.in/dashboard/CGP/RPT_CGP.aspx

https://www.pib.gov.in/PressReleasePage.aspx?PRID=1539258®=3&lang=2

CABINET

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2048607®=3&lang=2

PRESS INFORMATION BUREAU

https://www.pib.gov.in/PressReleseDetail.aspx?PRID=2187327®=3&lang=2

https://www.pib.gov.in/FactsheetDetails.aspx?Id=150473®=3&lang=2

OTHERS

https://pension.cg.gov.in/PensionRule_en.aspx

https://cpao.nic.in/pdf/NPS_ENGLISH_BOOK.pdf

https://pensionersportal.gov.in/pension/rules/ccspen1.htm

https://finance.maharashtra.gov.in/publication/%E0%A4%AE%E0%A4%B9%E0%A4%BE%E0%A4%B0%E0%A4%BE%E0%A4%B7%E0%A5%8D%E0%A4%9F%E0%A5%8D%E0%A4%B0-%E0%A4%A8%E0%A4%BE%E0%A4%97%E0%A4%B0%E0%A5%80-%E0%A4%B8%E0%A5%87%E0%A4%B5%E0%A4%BE-%E0%A4%A8%E0%A4%BF/

Click here to see pdf

PIB Research

(Release ID: 2258761)

Visitor Counter : 2550