Ministry of Finance

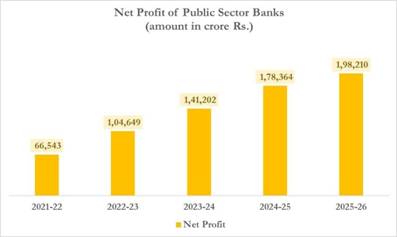

Public Sector Banks (PSBs) record an all-time high net profit of ₹1.98 lakh crore in FY 2025–26, marking the fourth straight year of profitability

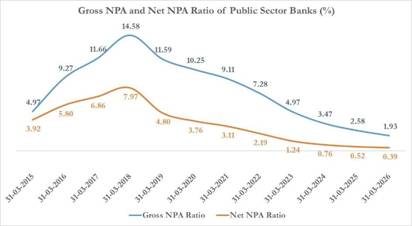

PSBs registered lowest ever NPAs - Asset quality improved significantly, with the Gross NPA ratio declining to 1.93% and the Net NPA ratio dropping to 0.39% as of 31 March 2026 — the lowest levels record historically

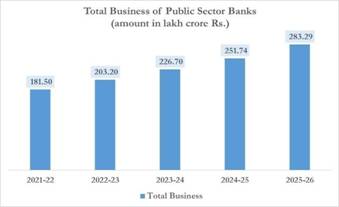

PSBs’ total business reached ₹283.3 lakh crore in FY 2025–26, registering robust y-o-y growth of 12.8%

Gross advances of PSBs grew by 15.7% y-o-y to ₹127 lakh crore as on 31.03.2026, with strong growth across Retail, Agriculture and MSME segments

Continued reforms and strengthened governance practices have reinforced PSBs through healthier balance sheets, enhanced operational resilience, and strong capital adequacy

Posted On:

12 MAY 2026 2:32PM by PIB Delhi

Public Sector Banks (PSBs) continued to register strong financial performance during FY 2025–26, reflecting sustained business growth, improved asset quality, record profitability and strong capital position. The improved performance demonstrates the resilience, stability and enhanced institutional capacity of PSBs in supporting the credit needs of a fast-growing Indian economy.

The aggregate business of PSBs increased to ₹283.3 lakh crore as on 31.03.2026, registering growth of 12.8% over the previous year. Aggregate deposits rose by 10.6% y-o-y to ₹156.3 lakh crore, reflecting continued depositor confidence and strong resource mobilisation by PSBs. Gross advances registered growth of 15.7% y-o-y and reached ₹127 lakh crore, indicating sustained credit demand across sectors of the economy.

Credit growth in the Retail, Agriculture and MSME (RAM) segments remained broad based during FY 2025–26. Retail, Agriculture and MSME advances grew by 18.1%, 15.5% and 18.2%, respectively, reflecting the important role of PSBs in supporting entrepreneurship, strengthening financial inclusion, and enabling broad-based economic growth.

Asset quality of PSBs improved significantly during FY 2025–26, with Gross NPA ratio (Non-Performing Assets) declining to 1.93% and Net NPA ratio to 0.39% as on 31.03.2026, reflecting historically low levels of stressed assets. Further, each PSB maintained provisioning coverage ratio of above 90%, indicating prudent provisioning practices, improved underwriting standards, effective risk management mechanisms and strengthened balance sheet resilience.

Fresh slippages continued to decline during FY 2025–26, with slippage ratio reducing to 0.7%. Total recoveries, including recoveries from written-off accounts, stood at ₹86,971 crore, reflecting improved recovery mechanisms and better credit discipline across PSBs.

Improved asset quality, healthy credit expansion and higher income contributed to improved profitability of PSBs during FY 2025–26. Aggregate operating profit reached ₹3.21 lakh crore, while aggregate net profit increased by 11.1% y-o-y to a historic high of ₹1.98 lakh crore, marking the fourth consecutive year of aggregate profitability for PSBs.

The capital position of PSBs remained healthy, with aggregate CRAR (Capital to Risk (Weighted) Assets Ratio) improving to 16.6% as on 31.03.2026, supported by internal accruals, retained earnings and capital raising of ₹50,551 crore during FY 2025–26. The CRAR of all PSBs remained well above the regulatory requirement of 11.5%, providing adequate cushion for continued lending growth.

Operational efficiency of PSBs also improved during the year, with cost-to-income ratio improving to 49.67%, reflecting better cost management and gains from technology adoption and digital transformation initiatives.

The continued improvement in the performance of PSBs reflects the resilience of the Indian economy and the Government’s sustained reforms aimed at strengthening the banking sector through improved governance, technology adoption, enhanced credit discipline and wider access to formal credit. These measures have contributed to lower stressed assets, improved operational efficiency and stronger financial position of PSBs.

Today, PSBs are well-capitalised, profitable and institutionally stronger, enabling them to effectively support India’s growth aspirations and contribute meaningfully towards the vision of Viksit Bharat by 2047.

*****

AD

(Release ID: 2260203)

Visitor Counter : 8136