PIB Backgrounder

AI-Powered Financial Inclusion in India

Posted On:

13 MAY 2026 11:23AM by PIB Delhi

|

Key Takeaways

|

- Digital Public Infrastructure and Artificial Intelligence provide the backbone for scalable and secure AI-led financial services.

- ULI enables digital access to multiple data sources and UPI allows for instant money transfers between any two bank accounts via a mobile platform.

- The “Banking BHASHINI” model to be developed that integrates banking vocabulary, regulatory guidelines, and industry-specific applications.

- Enabling Framework for Regulatory Sandbox fosters responsible innovation, enhance efficiency, and benefit consumers in the fintech sector.

- AI-powered solutions move beyond conventional credit scoring models and reduce reliance on informal lending by MSMEs.

|

Reimagining Financial Inclusion in a Digital-First Economy

India’s financial inclusion journey is undergoing a paradigm shift, driven by the convergence of a strong Digital Public Infrastructure (DPI) and Artificial Intelligence (AI). What began as an effort to expand basic banking access has evolved into a technology-led ecosystem focused on delivering intelligent, inclusive, and real-time financial services at scale. Leveraging vast digital footprints, advanced analytics, and consent-based data-sharing frameworks, AI is transforming how financial services are designed and delivered- enhancing efficiency, expanding outreach, and enabling more personalized financial solutions.

The transformation is particularly impactful for the underserved and “new-to-credit” segments, including MSMEs, informal workers, rural populations, and women-led enterprises. By reducing information asymmetries and moving beyond traditional credit assessment models, AI is unlocking access to formal finance, strengthening risk management, and improving financial resilience. As India advances towards a digitally empowered economy, AI is not only accelerating financial inclusion but also reshaping the financial ecosystem into one that is more responsive, secure, and future-ready.

Digital Solutions Transforming Financial Access

Financial inclusion is the process of ensuring access to financial services, with timely, adequate and affordable credit primarily for vulnerable groups such as weaker sections and low-income groups. In India, this has evolved from a policy goal into a digital-first reality. Over the past decade, a suite of interoperable digital platforms has transformed financial access from a policy objective into a scalable, technology-driven reality.

This transformation is anchored in foundational systems enabling identity verification, seamless payments, and direct benefit delivery. These systems ensure that financial services are accessible, affordable, and efficient across geographies. Together, they form the backbone of an integrated ecosystem that supports last-mile connectivity and future innovations.

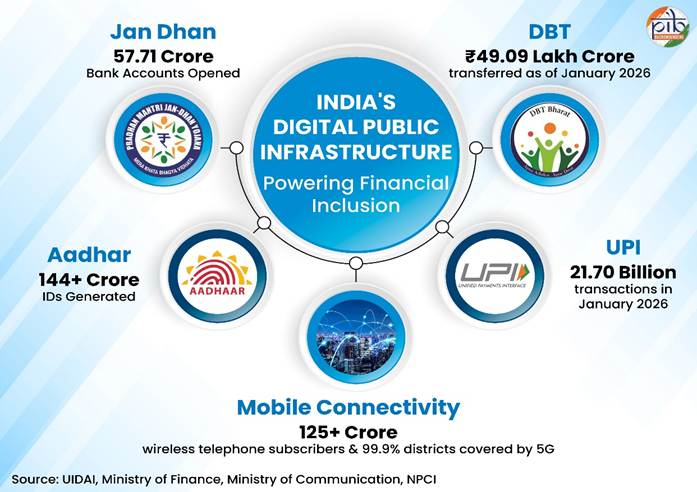

JAM Trinity (Jan Dhan-Aadhaar-Mobile)

JAM is a foundational convergence of universal bank accounts, biometric identity, and mobile connectivity. Its motive is to provide every citizen with a unique financial identity and a direct link to the state, ensuring that geography is no longer a barrier to financial access.

- As of March 2026, over 144 crore Aadhaar numbers have been generated for secure authentication.

- Jan Dhan accounts have grown to 58.16 crore (As of 29 April 2026) from 14.72 crore in 2015, with cumulative deposits totaling ₹3.02 lakh crore (As of 29 April 2026), bringing the unbanked into the formal economy.

- Mobile connectivity completes the triangle, with 125.87 crore wireless telephone subscribers and 5G mobile services covering 99.9% of districts, covering 85% of the population.

Unified Payments Interface (UPI)

UPI is a real-time payment system that allows for instant money transfers between any two bank accounts via a mobile platform. It aims to democratize digital payments by offering a low-cost, interoperable, and secure experience for both small merchants and individual users.

- In March 2026, approx. ₹29.53 lakh crore worth of 2,264.11 crore UPI transactions were carried out on the Unified Payment Interface (UPI).

- With 691 banks live on the platform, it accounts for nearly 81% of total retail payment volume in India, becoming the primary digital rail for both person-to-person and person-to-merchant payments.

Direct Benefit Transfer (DBT)

Under DBT system, government subsidies and welfare benefits are directly transferred into the bank accounts of beneficiaries. Its primary goal is to enhance transparency and efficiency by removing intermediaries, thereby eliminating leakages and delays in the delivery of social welfare.

- The system has transferred a cumulative ₹49.09 lakh crore directly to citizens as of January 2026.

- By eliminating duplicate and fake beneficiaries, it has saved the government over ₹4.31 lakh crore.

Together, these digital systems have created a robust, interoperable, and data-rich financial ecosystem. Such strong digital foundation not only enables inclusive financial participation but also generates the data and infrastructure necessary for AI powered innovation in financial services.

Enabling AI in Finance: Policy Push and Ecosystem Support

The integration of AI in financial services, backed by digital solutions, is supported by regulatory innovation, institutional initiatives, and financial literacy programs. These efforts are designed to strengthen risk management and consumer protection while ensuring that technology remains inclusive. Numerous initiatives have been taken that represent the core of India’s policy-driven approach to creating a secure and inclusive AI-financial ecosystem:

- In February 2026, the Digital India BHASHINI Division (DIBD) and the RBI signed an MoU to collaborate on integrating BHASHINI’s language AI models to enhance multilingual access to banking and financial services.

- The initiative aims at promoting financial inclusion across India’s diverse linguistic landscape by providing multilingual access to banking services in all 22 scheduled Indian language, thus removing literacy and language barriers.

BhashaDaan collects speech, text, and translations from people across India and uses them to train AI systems.

|

- The MoU provides for the deployment of BHASHINI models within RBI’s ecosystem. The model uses linguistic datasets through the Bhashadaan initiative to ensure high contextual accuracy for complex financial terminology and regulatory language.

- DIBD and RBI will jointly develop a domain-specific language model for the banking industry, named “Banking BHASHINI,” to integrate banking vocabulary, regulatory guidelines, and industry-specific applications.

- By providing AI-powered solutions for communication and service delivery, it ensures that all citizens, regardless of language, can access essential services and information effectively.

- The Reserve Bank of India (RBI) introduced the Enabling Framework for Regulatory Sandbox (RS), to foster responsible innovation, enhance efficiency, and benefit consumers in the fintech sector.

- Based on FinTech Working Group recommendations, it offers a controlled environment for testing new products/services under regulatory supervision before wider deployment.

- The objective of the RS is to foster responsible innovation in financial services, promote efficiency and bring benefit to consumers.

- It enables fintech startups and banks to test solutions such as Application Program Interface (APIs) services, digital KYC, and Cyber security products.

- The framework allows regulators to assess the benefits and risks of new technologies while ensuring financial stability and consumer protection.

- Launched in December 2024 by the Reserve Bank Innovation Hub (RBIH), MuleHunter.AI is an advanced AI-powered tool designed to identify and mitigate "mule" bank accounts used in cybercrimes.

- Unlike traditional rule-based systems, it uses AI/ML-powered tool to analyze transaction patterns in real-time, detecting anomalies that indicate money laundering or illegal betting.

- Successful pilot tests with large public sector banks have shown encouraging results, leading the RBI to encourage wider adoption across the banking ecosystem to strengthen national financial security.

Mule accounts, frequently used to launder money and facilitate cybercrime, have consistently posed difficulties for traditional detection approaches.

|

- Mission Digital ShramSetu announced in October 2025, is a proposed national initiative to create an AI-driven ecosystem that makes technology accessible, affordable, and impactful for India’s 490 million informal workers.

- The mission harnesses AI, Blockchain, and Immersive Learning to dismantle structural constraints such as financial insecurity, limited market access, and lack of formal skilling.

- It empowers workers with digital platforms to amplify their skills and increase productivity, ensuring they are integrated into the mainstream economy with dignity, thus ensuring financial inclusion.

- By providing tools for social protection and real-time skill verification, the mission aims to turn the informal workforce into a primary driver for the Viksit Bharat 2047 vision.

Together, these policy initiatives ensure that AI adoption remains secure, inclusive, and transparent, aligning with India's long-term vision of a digitally empowered society.

AI-Based Credit Scoring: Expanding Access to Formal Credit

Digital advancements and AI are reshaping India’s credit ecosystem by strengthening credit assessment and expanding lending access. Traditionally, access to formal credit was limited by the lack of verifiable financial histories, particularly for MSMEs, informal workers, and first-time borrowers. AI-powered solutions move beyond conventional credit scoring models and leverage alternative data such as digital payment transactions, GST filings, bank statements, and utility payments to assess creditworthiness. By converting digital footprints into dynamic risk profiles, AI enables faster, more accurate, and cost-efficient underwriting decisions. Moreover, AI-driven credit models have the potential to unlock an estimated credit gap of USD 130-170 billion in economic value thereby, reducing reliance on informal lending by MSMEs.

Alternative Credit Scoring (AI-Led Lending)

For the millions of Indians without a CIBIL score, AI serves as the new gatekeeper to credit. By leveraging the Unified Lending Interface (ULI), AI models analyze "digital footprints" to assess risk. ULI is a technology-based initiative to make frictionless credit available to every Indian and to further the Government’s broader vision of digital empowerment, financial inclusion, and last-mile service delivery. It functions as a Digital Public Infrastructure (DPI) in the lending space, integrating financial institutions and data providers through a standardised, API-based framework to support efficient and inclusive credit assessment.

Digital Public Infrastructure (DPI) refers to interoperable digital systems- such as digital identity, payment platforms, and data exchange frameworks that enable secure and efficient service delivery.

Application Programming Interface (API) is a set of rules and protocols that allows different software applications to communicate and exchange data with each other.

CIBIL Score, issued by Credit Information Bureau (India) Limited (CIBIL), is a three-digit numeric summary of a user’s credit profile and loan-worthiness, based on past repayment behaviour and credit records.

|

- ULI enables digital access to multiple data sources, including authentication services, land records, satellite service, and other financial and non-financial datasets, to support loan processing.

- As of December 12, 2025, 64 lenders (41 banks and 23 NBFCs) have been onboarded onto the platform. These lenders are utilising over 136 data services across 12 different loan journeys.

- ULI is being expanded to include customers of Regional Rural Banks (RRBs) and District Central Co-operative Banks (DCCBs), enhancing credit access in rural and semi-urban areas.

Account Aggregator (AA) framework

Complementing these advancements is the Account Aggregator (AA) framework, introduced by the Reserve Bank of India as a financial data sharing system. The AA system enables consent-based, secure sharing of financial data across institutions, significantly reducing documentation requirements and turnaround time for loan approvals.

Account Aggregators (AAs) are NBFCs that facilitate the retrieval and consolidation of a customer’s financial information. They transfer data from one financial institution to another based on an individual's instruction and consent.

|

The AA Framework, allows users to aggregate their financial information (like bank accounts, investments, loans, etc.) from multiple sources and share it with service providers (e.g., lenders, wealth managers) for services like loan applications or financial planning. Registration with the AA ecosystem is entirely voluntary for users. Currently, the RBI has granted Certificates of Registration to seventeen companies to operate as Account Aggregators.

It caters to the expanding market adoption across banking, securities, insurance, and pension sectors. With over 2.6 billion accounts enabled to share data, a total of 252.9 million users have linked their accounts on the AA framework (as on 31st December 2025). Notably, the AA ecosystem is strengthening the digital credit infrastructure and enhancing the effectiveness of AI-based credit models.

Conclusion

India’s financial inclusion journey is transitioning from expanding access to enabling intelligent, AI-driven financial empowerment at scale. By leveraging advanced analytics, alternative data, and robust DPI, the focus is shifting towards deeper credit penetration, enhanced risk management, and stronger consumer protection. The evolving ecosystem anchored in collaborative efforts between regulators, financial institutions and fintechs, supported by frameworks such as the Account Aggregator is fostering a more transparent, efficient, and inclusive financial system.

As India advances towards its Viksit Bharat 2047 vision, AI-led financial inclusion is set to play a pivotal role in driving sustainable economic growth, positioning the country as a global leader in building a resilient, future-ready financial architecture.

References

Ministry of Finance

https://financialservices.gov.in/beta/en/account-aggregator-framework

https://www.pmjdy.gov.in/home

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2139039®=3&lang=2

https://cga.nic.in/Page/Direct-Beneficiary-Transfer-DBT.aspx

Ministry of Electronics & IT

https://www.psa.gov.in/CMS/web/sites/default/files/publication/WEF_Transforming_Small_Businesses_2025.pdf?utm_source

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2232343®=3&lang=2

https://bhashini.gov.in/about-bhashini

https://bhashini.gov.in/

National Payments Corporation of India

https://www.npci.org.in/

Reserve Bank Of India

https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/FREEAIR130820250A24FF2D4578453F824C72ED9F5D5851.PDF

https://rbidocs.rbi.org.in/rdocs/Publications/PDFs/0RTP291220258C89B9E5F3F240AEB82AC25A1707A8C6.PDF

https://www.fidcindia.org.in/wp-content/uploads/2019/06/RBI-ENABLING-FRAMEWORK-FOR-REGULATORY-SANDBOX-28-02-24.pdf

https://fintech.rbi.org.in/FS_Publications?id=1262#C2

https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=59245

https://www.rbi.org.in/commonman/Upload/English/Content/PDFs/English_16042021.pdfhttps://www.rbi.org.in/commonman/Upload/English/Content/PDFs/English_16042021.pdf

NITI Aayog

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2176362®=3&lang=2#:~:text=To%20address%20this%2C%20NITI%20Aayog%20has%20called,increase%20productivity%2C%20and%20ensure%20dignity%20in%20work

India AI

https://indiaai.gov.in/article/rbi-s-ai-initiative-mulehunter-ai-ai-solution-to-tackle-digital-fraud-in-india

International Organisations

https://documents1.worldbank.org/curated/en/099031325132018527/pdf/P179614-3e01b947-cbae-41e4-85dd-2905b6187932.pdf

https://www.undp.org/digital/digital-public-infrastructure

PIB Archives

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2235812®=3&lang=1

See In PDF

***

PIB Research

(Release ID: 2260497)

Visitor Counter : 5182