PIB Backgrounder

Strengthening Rural Credit for Inclusive Growth in India

Posted On:

16 JUL 2026 11:05AM by PIB Delhi

|

India’s rural credit system is a key pillar of rural development and agricultural growth. It supports agriculture, allied activities, rural enterprises, and household consumption needs. Over time, the system has evolved from informal lending to a diversified institutional framework. Institutions such as NABARD, commercial banks, regional rural banks, cooperative banks, and small finance banks drive rural credit delivery. Recent surveys indicate improving rural economic conditions and expanding access to formal credit. Policy measures have strengthened the availability of affordable and timely credit. Key initiatives include priority sector lending, ground level credit targets, and the modified interest subvention scheme. Government policies and programmes have expanded rural credit through institutional reforms, digital platforms and financial inclusion, improving access to formal finance and strengthening rural livelihoods and economic growth.

|

India’s Rural Credit Landscape

India's rural credit ecosystem has expanded significantly over the years. It provides timely and affordable finance for agriculture, allied sectors, rural enterprises and households, supporting inclusive rural development. It meets short-term, medium-term and long-term credit requirements for both production and consumption. By supporting income generation, asset creation and household resilience, rural credit has become a key driver of rural development. It is delivered through a network of institutional sources, including Scheduled Commercial Banks, Regional Rural Banks, Cooperative Banks and the National Bank for Agriculture and Rural Development (NABARD), alongside non-institutional sources.

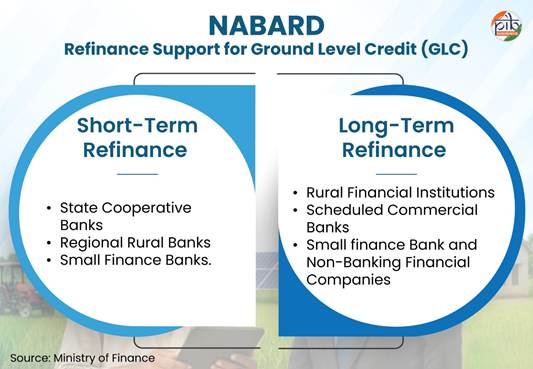

At the centre of this ecosystem is NABARD, the apex development financial institution for agriculture and rural development. It strengthens the rural credit architecture through refinance support, rural infrastructure financing, institutional development and supervision of Cooperative Banks and Regional Rural Banks. The growing reach of formal rural finance is reflected in NABARD's Rural Economic Conditions and Sentiments Survey (May 2026). About 77.2% of rural households reported higher consumption levels, reflecting rising purchasing power and sustained demand. Access to formal credit has also expanded significantly. Around 51% of households relying exclusively on formal sources and over 27% accessing both institutional and non-institutional channels.

Building on this strong institutional foundation, India's rural credit system has evolved from conventional banking to a technology enabled and inclusive ecosystem. Policy reforms, digital innovations and financial inclusion measures have improved access to institutional finance, enhanced the efficiency of credit delivery and reduced dependence on informal borrowing. Together, these efforts are strengthening agricultural growth, improving rural livelihoods and building a more resilient rural economy.

Evolution of Rural Credit System

India’s rural credit system has transformed into a more formal and diversified institutional framework. In the post-Independence period, the Government and the Reserve Bank of India (RBI) undertook key initiatives to strengthen institutional credit. These were among the earliest efforts to expand rural banking and support agricultural financing.

1955: The National Agricultural Credit (Long-term Operations) Fund was created and the State Bank of India was established. These initiatives marked a major step towards expanding rural banking and strengthening agricultural finance.

1969: 14 major commercial banks were nationalised. It reoriented banking policies towards priority sectors, particularly small farmers, which enhanced the flow of institutional credit to rural areas.

1982: NABARD was established, strengthening the rural credit architecture. It celebrated its 45th foundation day on 12th July 2026. It integrated financing, developmental, and supervisory functions for agriculture and rural development. NABARD also promotes financial inclusion, prepares district credit plans and supports Government initiatives aimed at expanding access to formal finance.

1992: The Self-Help Group (SHG)-Bank Linkage Programme was introduced which expanded access to formal credit for rural households.

1998: The Kisan Credit Card (KCC) Scheme improved the availability of timely and affordable credit for farmers.

2014: Pradhan Mantri Jan Dhan Yojana (PMJDY) was launched to expand financial inclusion through universal banking access, supporting credit, insurance and Direct Benefit Transfers. It forms a key pillar of the JAM (Jan Dhan–Aadhaar–Mobile) Trinity. This has transformed the delivery of welfare benefits through digitally enabled, transparent and targeted service delivery.

2015: The MUDRA Scheme (PMMY) was launched to provide collateral-free institutional credit to non-corporate, non-farm small and micro enterprises. This promotes rural entrepreneurship and self-employment.

2022 onwards: Digital initiatives such as the Jan Samarth Portal, e-KCC and others have transformed rural credit delivery through technology-enabled, accessible and inclusive financial services.

Institutional Architecture of Rural Credit

A strong institutional network underpins India's rural credit system. It plays a vital role in expanding access to formal finance and promoting inclusive rural development.

Scheduled Commercial Banks (SCB)

SCBs have significantly strengthened financial inclusion by expanding access to formal banking services. They deliver banking services through branches, Business Correspondents, digital platforms, and Government initiatives such as PMJDY and Direct Benefit Transfer (DBT). SCBs include public sector banks, private sector banks, foreign banks, payment banks, regional rural banks and small finance banks.

|

A SCB is a bank included in the Second Schedule of the RBI Act, 1934. These banks are eligible for loans at the bank rate from the RBI and are members of the clearing house.

|

At present, around 120 SCBs are providing banking services across the country.

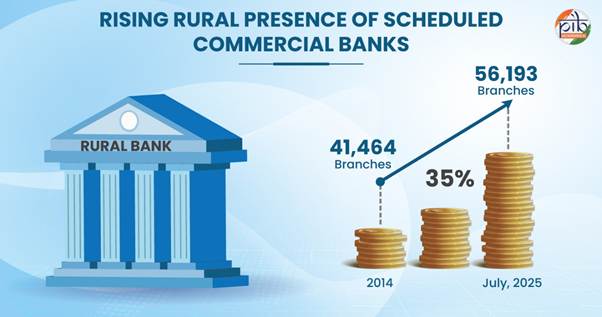

In rural areas, there were 41,464 SCB branches in 2014. This increased by over 35% to 56,193 rural branches by July 2025, playing a vital role in rural credit delivery.

Regional Rural Banks (RRBs)

RRBs were established under the RRB Act, 1976, with the objective of strengthening institutional credit in rural areas. They focus particularly on small and marginal farmers, agricultural labourers, artisans, and small entrepreneurs. Since inception, RRBs have played a critical role in promoting rural development and financial inclusion. Currently, 28 RRBs operate across States and Union Territories, having a branch network of over 22,000 in 700 districts.

Co-operative Banks

The co-operative banking system forms an integral part of India’s financial system, with separate urban and rural segments. While urban cooperative banks operate as a single-tier system, rural cooperative credit institutions follow a multi-tier structure. Based on their structure, there are different types of cooperative banks, including:

- State Co-operative Banks (StCBs),

- District Central Co-operative Banks (DCCBs),

- Primary Agricultural Credit Societies (PACSs),

- State Co-operative Agriculture and Rural Development Banks (SCARDBs),

- Primary Co-operative Agriculture and Rural Development Banks (PCARDBs).

These institutions have played an important role in expanding institutional credit by promoting banking habits among the poor in remote areas. As per RBI and NABARD, the co-operative network includes 1,458 Urban Cooperative Banks, 34 StCBs and 352 DCCBs.

Small Finance Banks (SFB)

SFBs were introduced following the Union Budget 2014–15. Licensed by RBI, SFBs aim to promote financial inclusion by providing accessible and secure savings facilities. They particularly focus on the unserved and underserved sections of the population. SFBs extend credit to small businesses, small and marginal farmers, micro industries, and other entities in the unorganised sector. These services are delivered through technology-driven, low-cost operations. At present, 11 Small Finance Banks are operational in the country.

These institutions collectively constitute the core of India's rural credit system, enabling wider access to formal finance and supporting inclusive development.

Policy Framework for Rural Credit

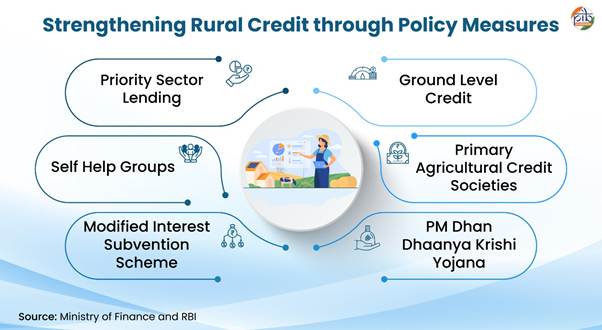

The policy framework for rural credit comprises various measures to ensure uninterrupted credit flow for rural development initiatives.

Priority Sector Lending (PSL)

Priority Sector Lending (PSL) is a mandatory framework set by the RBI. It requires banks to allocate a specific percentage of their total loans to critical or underserved sectors of the economy that struggle to access formal credit. This aims to ensure equitable distribution of credit.

The guidelines apply to Commercial Banks, including RRBs, SFBs, Local Area Banks, and Primary (Urban) Cooperative Banks (excluding Salary Earners’ Banks). These banks are mandated to allocate credit to agriculture. At least 18% of their Adjusted Net Bank Credit or Credit Equivalent of Off-Balance Sheet Exposures, whichever is higher, must be earmarked for this purpose.

Adjusted Net Bank Credit = Net Bank Credit + investments made by banks in non-SLR bonds held in HTM category

|

Within this, a sub-target of 14% is prescribed for non-corporate farmers and 10% for small and marginal farmers. Concessional refinance is provided to eligible Rural Financial Institutions (RFIs) through various funds created out of PSL shortfall. These include Short-Term Cooperative Rural Credit Fund (STCRCF), Short-Term RRB Credit Refinance Fund (STRRBF) and Long-Term Rural Credit Fund (LTRCF).

Ground Level Credit (GLC)

The Government sets annual GLC targets for agriculture and allied sectors, which banks must achieve each financial year. These targets are set region-wise, agency-wise, and by loan category, including crop and term loans. Since 2021-22, dedicated targets for allied activities like dairy, fisheries, and animal-husbandry have been introduced to enhance credit support.

During FY15-FY24 agricultural credit disbursement grew at over 13% annually, reflecting increasing financial support to the sector. For FY 2025-26, the GLC target was ₹32.50 lakh crore, with a sub-target of ₹ 5.0 lakh crore for Animal Husbandry, Dairying and Fisheries farmers. This marks more than fourfold increase from ₹8 lakh crore in FY 2014–15, reflecting effective targeted credit policies.

To enhance GLC in agriculture, NABARD provides refinance support to banks to supplement their resources for short-term and long-term lending to agriculture and allied sectors.

Self Help Group (SHG)

The Self-Help Group–Bank Linkage Programme (SHG-BLP), was initiated by NABARD. It was launched to connect rural Self-Help Groups (SHGs) with the formal banking system, enabling access to affordable institutional credit and other financial services. The programme has emerged as an effective model for integrating the formal financial sector with rural poor households. This has particularly benefitted women who traditionally lacked access to formal credit due to the absence of a credit history.

To further strengthen this ecosystem, the National Rural Livelihoods Mission (NRLM) was launched in 2010 by restructuring the erstwhile Swarnajayanti Gram Swarozgar Yojana (SGSY). Subsequently, NRLM was renamed as DAY-NRLM (Deendayal Antyodaya Yojana - National Rural Livelihoods Mission) w.e.f. March 29, 2016. The renaming further reinforced the SHG-Bank Linkage Programme, which received renewed momentum through the large-scale promotion and nurturing of women-led SHGs.

|

DID YOU KNOW?

10.05 crore rural women have been mobilised into more than 90.90 lakh SHGs till July 2025. It covers a large number of districts and blocks nationwide.

|

DAY-NRLM is a poverty alleviation programme. It organises rural poor households into SHGs and supports them in increasing incomes and improving their quality of life. The programme is being implemented across the country (except Delhi and Chandigarh). As of 10 July 2026, over 19.83 lakh SHGs are operational with loan disbursement of ₹13.28 lakh-crore recorded since inception.

This mission has also improved access to bank credit through the deployment of Bank Sakhis. They assist SHG members in opening bank accounts, preparing and submitting loan applications, and ensuring timely repayment. This has helped strengthen credit linkage and reduce NPAs. Around 50,548 Bank Sakhis have been deployed, supporting SHGs in accessing bank credit of over ₹12.18 lakh crore since 2013-14 (as on February, 2026).

Primary Agricultural Credit Societies (PACS)

PACS are the grassroots-level institutions of the short-term cooperative credit structure. They directly interact with rural borrowers, providing loans and facilitating repayment. PACS also undertake distribution and marketing functions for agricultural inputs and produce.

They form the base of the cooperative credit system. They also serve as the final link between borrowers and higher financing institutions, including SCBs and RBI/NABARD.

- In 2023, the Government approved a plan to establish 2 lakhs new multipurpose PACS, Dairy, Fishery Cooperative Societies. These will be set up across all panchayats over 5 years.

- So far, 32,836 new societies have been registered, and 15,793 dairy and fishery cooperatives strengthened as on 20 January 2026.

- Efforts to modernise PACS through digitisation are also underway. Out of 79,630 approved PACS, 61,842 PACS have successfully migrated to the Common ERP-based national software as of 10 March 2026.

Modified Interest Subvention Scheme (MISS)

MISS is a central sector scheme ensuring the availability of short-term credit to farmers at affordable interest rates through KCC. Under the scheme, farmers receive short-term loans at a subsidised interest of 7%, with 1.5% subvention provided to lending institutions. Farmers repaying loans promptly are eligible for an additional incentive of up to 3%, reducing the interest rate to 4%.

The Union Budget 2025–26 introduced several measures to strengthen MISS.

- Enhanced the loan limit under the MISS from ₹3 lakh to ₹5 lakh for loans availed through KCC.

- The lending limit for fisheries and allied activities increased from ₹2 lakh to ₹5 lakh.

- From January 2025, the limit for collateral-free short-term agricultural loans increased from ₹1.6 lakh to ₹2 lakh per borrower.

This measure aims to enhance financial access for farmers amid rising input costs and inflation. It enables them to meet operational and developmental needs without collateral.

PM Dhan Dhanya Krishi Yojana (PM-DDKY)

PM-DDKY, approved in July 2025, aims to catalyse growth in 100 low performing agri-districts. It adopts a saturation-based convergence of 36 Central schemes across 11 Ministries. A key objective of the scheme is to enhance access to short-term and long-term agricultural credit for farmers. The scheme also focuses on improving agricultural productivity and promoting crop diversification. It encourages sustainable agricultural practices and strengthens irrigation infrastructure for reliable water access. It further aims to augment post-harvest storage capacity at the panchayat and block levels. Committees are being formed at District, State and National level for effective planning, implementation and monitoring of the Scheme.

Based on cumulative output from inception to May 2026, the top-performing districts are:

- Banka, Bihar

- Mahoba, Uttar Pradesh

- Charaideo, Assam

- Kishanganj, Bihar

- Tikamgarh, Madhya Pradesh

Strengthening Rural Financial Inclusion

Financial inclusion is a key pillar of strengthening India's rural credit ecosystem. The Government has adopted a multi-pronged approach to strengthen rural credit and financial inclusion.

Kisan Credit Card

The KCC scheme was introduced as an innovative credit mechanism to provide adequate and timely credit support from the banking system. It offers features such as an ATM-enabled debit card and one-time documentation. It also provides in-built provision for cost escalation and flexibility for multiple withdrawals within the sanctioned limit.

Loans under KCC are provided to farmers for wide range of agricultural requirements, including:

- short-term crop cultivation

- post-harvest operations

- marketing-related expenses

- household consumption needs

- working capital for farm maintenance

- investment credit for allied and non-farm activities.

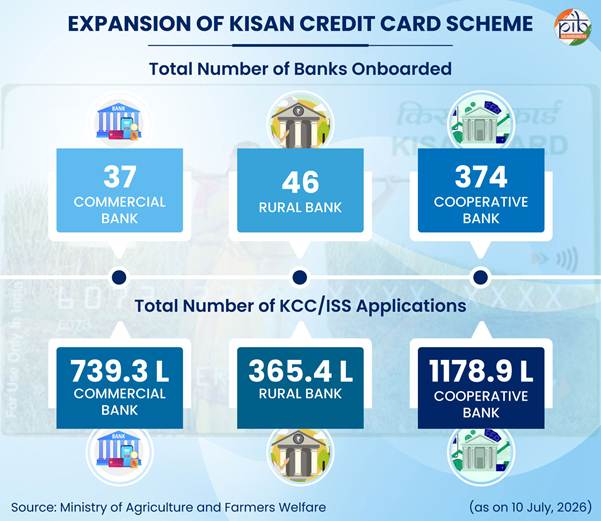

As on 8 July 2026, total KCC applications stand at ~739 lakh under commercial banks and more than 365 lakh under RRBs. Cooperative banks account for the highest number of applications at over 1178 lakh.

The scheme coverage expanded to include individual and joint borrowers who are owner cultivators, tenant farmers, oral lessees, and sharecroppers. It also covers Self-Help Groups (SHGs) and Joint Liability Groups (JLGs) of farmers. The scheme was further extended to allied sectors such as dairy, fisheries, and animal husbandry in 2019.

NABARD has also introduced the e-KCC portal for RRBs and RCBs, enabling end-to-end digitisation of the loan application process. Through this platform, farmers can submit applications without the need to visit bank branches. Additionally, the e-KCC facility allows farmers to apply for crop loans via nearby Common Service Centres (CSCs). It facilitates faster processing, enabling loan sanction within a short turnaround time of about 2 days.

The Government, RBI, NABARD and banks conduct financial literacy programmes to promote awareness of KCC benefits among farmers. These are delivered through Centres for Financial Literacy (CFLs) and Financial Literacy Camps (FLCs). In addition, the RBI organises Financial Literacy Week (FLW) annually to disseminate financial education among the public across the country.

Pradhan Mantri Jan Dhan Yojana (PMJDY)

PMJDY plays a key role in the development of marginalised communities. It provides universal banking access through at least one basic account per household. Besides, it offers access to credit, insurance, and pension. The scheme covers both rural and urban areas and offers RuPay debit cards to account holders. It supports the expansion of DBT by enabling government benefits to be transferred directly into bank accounts. Additionally, it links instruments such as KCC to the RuPay platform. As part of the Jan-Dhan-Aadhaar-Mobile (JAM) trinity, it provides a robust mechanism for delivery of subsidies and welfare benefits.

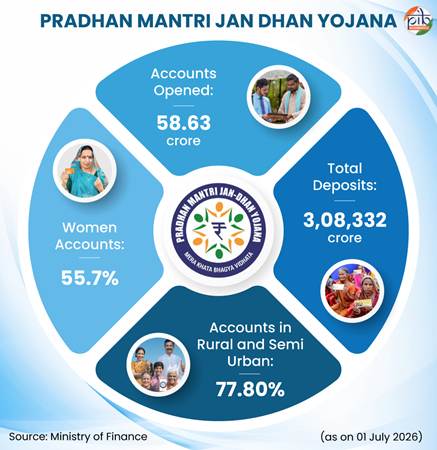

As on 24 June 2026, over 58.63 crore Jan-Dhan accounts have been opened, with deposits exceeding ₹3 lakh crore. Of these, 32.68 crore accounts (55.7%) belong to women, and 45.62 crore accounts (77.8%) are in rural and semi-urban areas.

Jan Samarth Portal

The Jan Samarth Portal, launched in June 2022, is a one-stop digital platform to link Government-sponsored loan and subsidy schemes, including KCC. The portal aims to expand the reach of government schemes and streamline credit delivery. It provides easy access to beneficiaries, financial institutions, and government agencies. The portal also promotes inclusive growth by guiding beneficiaries to suitable schemes through simple digital processes. It ensures end-to-end coverage of all linked schemes.

Jan Dhan Darshak App

The Jan Dhan Darshak App enables citizens to locate banking service points, including bank branches, ATMs, Bank Mitras and Common Service Centres (CSCs), across the country. It also helps the Government monitor banking access in villages.

- As of 6 March 2025, 99.92% of villages had a banking outlet within a 5 km radius.

- Additionally, villages in Dadra and Nagar Haveli have achieved full coverage.

Inclusive Growth Ahead

Over time, India’s rural credit system has transitioned from an informal structure to a diversified, institution-led and policy-driven framework. Supported by institutions and targeted policies, the system has reinforced rural prosperity to timely and affordable credit across agriculture and allied sectors.

With increasing digitisation, improved institutional reach, and financial inclusion, the rural credit ecosystem is becoming more accessible and efficient. This is contributing to inclusive rural development and long-term economic growth in the country.

References

Ministry of Finance

https://www.pmjdy.gov.in/account

https://www.nabard.org/auth/writereaddata/tender/pub_1703261242421830.pdf?csrt=8538899789072578698

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2049231®=48&lang=2

https://financialservices.gov.in/beta/en/nabard-act

https://financialservices.gov.in/index.php/nabard

https://financialservices.gov.in/banking

https://www.nabard.org/contentsearch.aspx?AID=225&Key=shg+bank+linkage+programme

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2246855®=3&lang=1

https://financialservices.gov.in/beta/en/banking-faq

https://financialservices.gov.in/beta/en/banking-overview#:~:text=The%20structure%20of%20the%20banking,the%20needs%20of%20the%20borrowers

https://financialservices.gov.in/beta/en/page/regional-rural-banks

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2246856®=3&lang=1

https://www.pib.gov.in/PressReleaseIframePage.aspx?PRID=2241257®=3&lang=2

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2098033®=3&lang=2

https://financialservices.gov.in/beta/en/agriculture-credit

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2241257®=3&lang=2

https://sansad.in/getFile/loksabhaquestions/annex/185/AU1365_spXbvr.pdf?source=pqals

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2246857®=3&lang=1

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2247026®=3&lang=2

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2240720®=3&lang=1

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2069170®=48&lang=2

https://www.pib.gov.in/PressReleaseDetail.aspx?PRID=2246855®=3&lang=2

RBI

https://www.rbi.org.in/upload/publications/pdfs/60618.pdf

https://rbidocs.rbi.org.in/rdocs/Publications/PDFs/0HBS2025290820256728B882492F427DA0262A1392E16E95.PDF

https://www.rbi.org.in/upload/Publications/PDFs/58848.pdf

https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12799

https://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=3657

https://www.rbi.org.in/commonman/English/Scripts/Notification.aspx?Id=2311

https://www.rbi.org.in/commonman/Upload/English/Notification/PDFs/NOTI1406072017.PDF

https://www.rbi.org.in/commonman/english/scripts/Notification.aspx?Id=794#:~:text=(iv)%20The%20targets%20and%20sub,may%20use%20current%20exposure%20method.

Ministry of Cooperation

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2157875®=3&lang=2

http://cooperation.gov.in/en/about-primary-agriculture-cooperative-credit-societies-pacs

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2245119®=48&lang=2

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2146717®=3&lang=2

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2222743®=3&lang=1

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2238404®=3&lang=1

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2145219®=48&lang=2

Ministry of Agriculture & Farmers Welfare

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2131989®=3&lang=2

https://fasalrin.gov.in/

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2099696®=48&lang=2

Ministry of Fisheries, Animal Husbandry and Dairying

https://sansad.in/getFile/annex/267/AS338_apRnsi.pdf?source=pqars

Ministry of Rural Development

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2146872®=3&lang=2

https://banklinkage.lokos.in/

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2224571®=3&lang=1

https://www.pib.gov.in/PressReleseDetailm.aspx?PRID=2237490&utm

https://www.myscheme.gov.in/schemes/day-nrlm

Prime Minister’s Office

https://www.pmindia.gov.in/en/major_initiatives/pradhan-mantri-jan-dhan-yojana/

NABARD

https://www.nabard.org/auth/writereaddata/WhatsNew/pub_1805261242421311.pdf?csrt=5126807064223528344

Sansad

https://sansad.in/getFile/loksabhaquestions/annex/186/AU2461_E8kYRN.pdf?source=pqals

https://sansad.in/getFile/loksabhaquestions/annex/185/AU3857_Sk64qF.pdf?source=pqals

Niti Aayog

https://pmddky.niti.gov.in/aboutTheScheme

https://pmddky.niti.gov.in/dashboard

World Bank

https://documents1.worldbank.org/curated/en/127451468315304370/pdf/327300PAPER0P01Finance1ESW01PUBLIC1.pdf

https://documents1.worldbank.org/curated/en/486171590655967465/pdf/SHG-Bank-Linkage-A-Success-Story.pdf

PIB Headquarters

https://www.pib.gov.in/PressNoteDetails.aspx?NoteId=154909&ModuleId=3®=3&lang=2

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2181702®=3&lang=2

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2238004®=48&lang=2

Others

https://www.smspup.in/ajaturjkerkejk16778j/2112202325543mba%20april%202023-65-83.pdf

https://www.ijarse.com/images/fullpdf/1491815847_P550-555.pdf

https://icrier.org/pdf/22dec/ramanathan_issuespaper.pdf

https://epwrf.in/includefiles/c10652.htm?utm

https://ies.gov.in/arthapedia/concept/priority-sector-lending-psl

https://www.rfilc.org/library/rural-finance-today-advances-and-challenges/

Click here to see pdf

***

PIB Research

(Release ID: 2285236)

Visitor Counter : 1223